This article is the first in a three-part series under SFOC’s Explained column examining the role of public and private financing in the LNG carrier industry, as well as its environmental impacts.

As countries across the world search for cleaner ways to generate electricity, one widely promoted solution is liquefied natural gas (LNG). Often described as the ideal “bridge fuel” for nations seeking to move away from oil and coal, this energy source accounts for a significant share of global power generation – around 15% of global gas consumption and 23% of total energy supply in 2024.

However, since this gas can only be found in certain parts of the world, it must often be transported thousands of miles by sea to reach the markets that depend on it. That journey is made possible by gigantic, highly specialized vessels known as LNG carriers (LNGCs), purpose-built to carry millions of gallons of super-cooled gas across oceans. Put simply, LNGCs function as the physical backbone of the global LNG trade.

Yet, despite their importance, these ships are seldom the subject of public debate. They move across jurisdictions, operate far from shore, and benefit from the widely accepted “LNG = clean energy” myth, despite mounting proof of significant lifecycle emissions and a massive environmental footprint. Even less visible is the financial architecture keeping them afloat. At production costs of hundreds of millions of dollars each, without financing from private banks, most LNG carriers would never leave the drawing board.

As Annual General Meeting (AGM) season approaches for the private banking sector, one question remains yet to be answered: why, despite growing evidence that new fossil fuel infrastructure is undermining net-zero goals, are private financial institutions still funding the expansion of LNG carrier fleets?

To make sense of such a question, we must first take a closer look at how LNG carriers work, why fleets are expanding despite obvious signals to divest, and how LNGC financiers are risking more than just emissions by refusing to do so.

What are LNG Carriers?

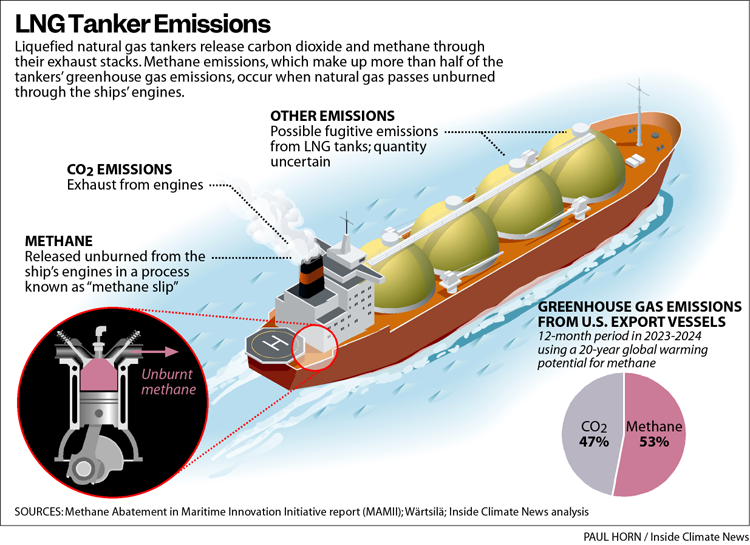

LNG carriers (LNGCs) connect gas-exporting countries with gas-importing ones. Their cargo, natural gas, is a fossil fuel composed of methane (CH₄), which is extracted via drilling and widely used for heating, electricity generation, and industrial activity.

For long-distance transport, the gas is cooled to around -162°C, reducing its volume by roughly 600 times and turning it into the liquefied state we know as LNG. LNG carriers, essentially floating cryogenic storage facilities, then transport LNG from Point A to Point B, maintaining extremely cold temperatures and stability during long ocean voyages where pipelines are unavailable or politically constrained.

LNG carriers are among the most expensive commercial ships in operation, typically costing about USD 250 million per ship and taking several years to build. For perspective, the Japanese city of Inagi, with a population of just under 100,000, operates on a general fund budget of about approximately USD 300 million - meaning a single LNG carrier costs nearly as much as an entire year of spending for a small city. And that’s not all. LNG carriers are designed to operate for 25 to 40 years, effectively locking in decades of fossil fuel infrastructure (read: more emissions) and long-term capital commitment.

When Money Talks: How Private Financing, Not Demand, Enables LNGC Expansion

Most assume the LNG carrier orderbook is packed to the brim because of rising electricity demand or some urgent need for natural gas, but this is rarely the case. At its core, the continued expansion of LNG carrier fleets is driven far more by available capital than by actual energy needs.

This dynamic is made possible because of how projects are financed. LNG carriers are highly leveraged assets, meaning they rely heavily on debt or loans to boost potential returns on an investment.

In any given case of a new LNGC project:

· 60–80% of construction costs are financed through debt

· Long-term charter contracts (often 20-30 years) are used to secure loans

· Export credit agencies provide guarantees and insurance

· Risk is distributed across banks, insurers, and leasing structures

Public guarantees take on part of the potential losses if projects underperform, reducing the risks faced by private investors. Structured finance arrangements then spread said risk across multiple institutions, further reducing potential fallout.

Export credit agencies, public financial institutions which help domestic companies trade their goods and services in overseas markets, further support LNGC deals by providing insurance and credit enhancements which lower borrowing costs and protect private lenders from losses.

These financial arrangements make LNG carriers appear stable and bankable investment vehicles. Since 2016, the world’s 60 largest banks have provided more than $6.9 trillion in fossil fuel financing with gas infrastructure and LNG continuing to receive substantial support despite net-zero pledges, thereby encouraging continued private investment.

In other words, finance creates supply.

The culprit? A self-reinforcing system in which private capital, supported by public de-risking mechanisms, enables LNG carrier expansion even when long-term energy pathways strongly indicate declining demand for fossil fuels.

The Three Blind Spots of LNG Carriers Expansion

Despite being portrayed as safe investments, LNG carriers face mounting structural risks.

1. Climate Misalignment Risk

The International Energy Agency’s Net Zero by 2050 scenario clearly states that under climate-aligned pathways, global gas demand must decline within the next decade - and that no new fossil fuel infrastructure is needed beyond projects already in progress.

Beyond this, the lifecycle emissions of LNG are significant, with methane leakage and methane slips during combustion and transport directly contributing to global warming. Methane, compared to CO2, has more than 80x the global warming potential (GWP) over a 20-year period. In addition, LNG shipping has serious negative consequences for marine biodiversity, contributing to underwater noise pollution affecting marine mammals, ballast water discharge facilitating the spread of invasive species, thermal pollution, and cumulative pressure on biodiversity hotspots.

A recent Cornell University study found that when production, liquefaction, shipping, and use are fully accounted for, the climate footprint of liquefied natural gas can be comparable to or even worse than coal. Yet, LNG carriers ordered today will likely operate well into the 2050s and 2060s, directly undermining net-zero goals, and these impacts remain largely excluded from financial risk assessments.

Financing these assets demonstrates the assumption of continued growth in gas demand: a trajectory incompatible with climate science.

2. Financial and Stranded Asset Risk

The LNG carrier market depends on long-term, stable gas demand to justify its high upfront costs. But in a net-zero scenario consistent with the 1.5°C goal, where global gas demand is set to drop by more than three-quarters by 2050, LNGC investors face growing risks of underutilization, contract renegotiation, reduced charter rates and early retirement.

The LNG carrier market is already experiencing oversupply cycles. As demand weakens in line with predictions, today’s high-cost vessels, with a 25-40 year operational lifespan, risk becoming stranded assets in the near future. Long-term contracts don’t eliminate this structural risk; they merely delay the moment when the financial cracks finally reach the surface.

3. Reputational and Policy Risk

Many large private banks have adopted net-zero commitments and introduced sectoral exclusion policies, often targeting coal and, in some cases, upstream oil and gas in an attempt to align with growing climate risks.

But a major blind spot remains: midstream fossil fuel assets, including LNG shipping.

LNG carriers frequently fall outside exclusion policies, climate screening frameworks, and green taxonomy restrictions. This gap allows banks to maintain climate-aligned narratives while continuing to finance fossil fuel transport infrastructure. This oversight inevitably creates a loophole where banks restrict extraction but continue financing the transport systems that make fossil fuel expansion viable.

LNG Expansion in Action: The Mozambique Case

The environmental impacts of LNG shipping are especially pronounced in regions like the Mozambique Channel, a globally important marine biodiversity hotspot and a key habitat for whales, coral reefs, and migratory species. LNG carrier traffic in this area has risen sharply due to large-scale LNG export projects, increasing underwater noise, ballast water discharge, and localized pollution along fixed shipping routes.

The restart of major gas development projects in northern Mozambique, despite past instances of violence, forced displacement and unresolved social and security concerns, has further intensified pressure on both marine and coastal environments. For coastal communities, this expansion has translated into declining fish stocks, disrupted traditional livelihoods, and the gradual loss of marine ecosystems that have supported local populations for generations, while the benefits of LNG development largely flow elsewhere.

How Civil Society is Pushing Back

On December 10th 2025, Human Rights Day, SFOC joined partners in Paris to stage a public demonstration in front of French private bank Crédit Agricole, bringing attention to the bank’s continued role in financing the LNG value chain, including LNG carriers, despite raising concerns about the climate and social harms linked to projects such as Mozambique LNG.

The action called on Crédit Agricole to stop supporting LNG projects and associated shipping infrastructure that lock in decades of fossil fuel dependence and emissions. In doing so, the mobilization highlighted that banks financing LNG carriers are not neutral intermediaries but key enablers making LNG expansion projects both viable and profitable. With AGMs on the horizon, shareholders and stakeholders are increasingly questioning whether these decisions are worth the risks – climate, reputation and finance-wise. Private banks need to be able to answer them.

Why LNG Carriers Matter Now

LNG carriers sit at a critical leverage point in the fossil gas system. Without them, global LNG trade cannot expand. And without financing, most new carriers would not be built.

For banks serious about aligning with climate science and reducing potential stranded asset risks, LNG shipping can no longer remain outside the scope of scrutiny.

Should LNG shipping continue to be financed without robust assessment of climate compatibility, biodiversity impacts, and long-term financial exposure, net-zero commitments risk becoming rhetorical rather than operational. The question for private financiers this AGM season then becomes this: can a transition strategy be credible if it ignores the ships that make fossil fuel expansion possible?

The answer is pretty clear.

Understanding private capital flows is only half of the story. In our next Explained blog, we’ll explore how public finance mechanisms are enabling, guaranteeing and legitimizing continued LNG expansion, inevitably delaying a full fossil fuel phaseout.

Happy reading!

Related insights

Advancing the Transition Away from Fossil Fuels

Key Outcomes from Santa Marta

2026-05-29

Explained: How LNGC Shipowners Fuel Harm Thousands of Miles Away

How the LNGC industry's weak environmental standards are destroying ecosystems and livelihoods

2026-05-13

Miles to be Heard by Those Who Never Had to Live Downstream: UBS's Exposure to Thai Energy Projects Flagged at the AGM

Thai villager carried years of struggle to UBS's doorstep.

2026-05-11

Explained: The Public Finance Mechanisms Keeping the LNG Carrier Industry Afloat

How Government Funds are De-risking LNGC Expansion

2026-04-02

Hyundai Has a Chance to Lead Asia’s Auto Transition — But Time Is Running Out

Time is running out for Hyundai to match Its EV success with climate transparency

2025-09-23

World Environment Day, June 5

#BeatPlasticPollution: A Climate Imperative

2025-06-05

Financing the Climate Crisis: South Korea’s Global Fossil Fuel Footprint

The Role of Public Financing Institutions in the Age of Climate Change

2025-06-04

Navigating the Blue Future: SFOC at the 2025 Our Ocean Conference

Busan, Korea (April 28 - 30, 2025)

2025-05-08

IMO Approves First-Ever Global Carbon Pricing for Shipping — But Is It Enough?

MEPC 83 Marks a New Era in Shipping Decarbonization, Yet Falls Short in Ambition

2025-04-25

Green Promises, Dirty Money: The Silent Support Behind KEPCO’s Fossil Expansion

KEPCO’s Investors and Underwriters: Ignoring the Warnings, Enabling the Problem

2025-04-10

Retracing the Steps of the LNG Trade: Why Canada's First Nations Came to Korea

The LNG Boom is "Good News"...for Whom?

2025-03-13

International Shipping Industry’s Passage to Net-Zero by 2050

What really happened at the MEPC 82?

2024-10-11

True Climate Impact of LNG Carriers

A comprehensive lifecycle emission analysis of LNG, enabled by LNG carriers

2024-10-11

Floating Pipelines Fuelling the Fossil Fuel Crisis: LNG Carriers

2024-09-01