This article is the second in a three-part series under SFOC’s Explained column examining the role of public and private financing in the LNG carrier industry, as well as its environmental impacts.

In our last LNGC Explained blog, we took a look at what liquefied natural gas carriers (LNGCs) are, and how financing from banks and other private financial institutions secures their continued production despite a massive supply glut and a growing environmental footprint. This time around, we examine the role of public finance – i.e. government money – in enabling, guaranteeing and legitimizing continued LNG expansion, inevitably delaying a full fossil fuel phaseout.

How Public Finance Enables LNGC Expansion

Besides private finance flows like the ones discussed previously, the bulk of LNGC financing is funneled through public finance institutions (PFIs), government-owned structures designed to manage public investments, support policy implementation and fund activities and projects that contribute to a country’s economic growth. They function as providers of “long-term finance, credit facilities and financial services” directed towards key sectors like agriculture and industry, including energy projects.

PFIs include Export Credit Agencies (ECAs), which help domestic companies trade their goods and services in overseas markets; multilateral development banks (MDBs), international banks funded by several countries to support development projects; and bilateral development banks (BDBs), funded by a single country to assist projects in partner nations.

In practice, PFIs have played a central role in enabling fossil-fuel expansion by covering risks that private financiers are unwilling to bear. Through insurance, credit guarantees and loans, they mobilize substantial co-financing, extending a lifeline for risky fossil-fuel projects. Public finance plays a critical enabling role in LNG carrier expansion, particularly during the construction stage. Major shipbuilders work closely with PFIs to secure direct loans and guarantees for LNGC projects.

Even as ECAs withdraw from oil and gas, their support for LNG infrastructure continues. ECAs safeguard shipbuilders’ interests by reducing financing costs for shipowners and commercial banks, allowing projects to proceed even with long-term climate and demand risks present. They serve as a financial pillar for projects that would have otherwise struggled to secure funding, offering risk mitigation solutions and insurance. ECA involvement typically makes lending cheaper for shipowners and operators, providing stability in a maritime sector prone to cyclical downturns.

How Public LNGC Financing Undermines Climate Goals

As we discussed last time, LNG, via these massive carriers, typically travels much longer distances than pipeline gas. Despite being cooled to temperatures as low as -162°C, LNG still has significant climate impacts even in its liquefied form: its main component, methane, is a powerful climate pollutant responsible for a third of net warming since the Industrial Revolution. Methane leakage can cause fires, generate smog, affect health and accelerate global warming. The further LNG travels, the more methane can potentially escape, significantly increasing the LNG shipping sector’s methane emissions intensity.

Curbing methane emissions is largely recognized as one of the most effective near-term means of keeping the 1.5°C goal within reach. According to the IPCC’s 2023 report, staying within this range requires cutting methane emissions by a third by 2030 and halving them by 2050. The LNG shipping industry risks undermining these targets, despite numerous findings indicating no new LNG carriers are needed, describing LNGC expansion as deeply incompatible with both the IEA’s Net Zero Emissions (NZE) pathway and already adopted national policies falling under the Stated Policies Scenario (STEPS) umbrella.

At COP26 in 2021, the U.S. and European Union launched the Global Methane Pledge (GMP), through which 159 countries, including top shipbuilders like South Korea and Japan, have agreed to reduce global methane emissions by at least 30% from 2020 levels by 2030. Yet, in spite of these climate commitments and mounting evidence against further expansion, public finance continues to pour billions into LNGC projects, keeping this heavy-emitting industry afloat. The global LNG shipping sector continues to witness unprecedented growth, with fleet capacity almost tripling over the past decade. As PFIs’ investments persist, stranded asset and carbon lock-in risks grow, further derailing the sector’s decarbonization trajectory.

Murky Waters: How Opaque Reporting and Ambiguous Finance Frameworks Greenwash LNG

LNG investment persists under the pretense of sustainability thanks to financial institutions’ selective reporting of information and channeling of funds via private subsidiaries. This is often enabled by faulty green finance frameworks – national, regional and international strategies, financial instruments and policies designed to encourage and justify the financing “transition-aligned”, “sustainable” or “green” projects. These frameworks vary in scope, legal status and ambition; examples include MDB sustainability frameworks like the Asian Development Bank’s Strategy 2030, as well as shipping-focused initiatives like the European Investment Bank’s Green Shipping Guarantee Programme or the Poseidon Principles. In Europe, public institutions’ maritime LNG project funding is notably supported by the European Union’s directive on the deployment of alternative fuels infrastructure.

Guidelines on what constitutes green financing eligibility within the shipping sector are often murky and unexplicit. Current frameworks have often been criticized for labelling LNG as a “transition” or “green” fuel, despite its climate impacts. This ambiguity has effectively enabled the labeling of 14 maritime LNG projects as “green” over the last decade.

The water gets murkier when it comes to where investment decisions are being made. In certain cases, loan structures, memoranda of understanding, credit facilities and wider finance frameworks are put together by ECAs and MDBs to support “alternative fuels and cleaner technology”, “green investments”, “growth and decarbonization” or “sustainable shipping efforts”. These institutions can then pass financial responsibility and decision-making authority to private actors or intermediaries, with little oversight. In the end, this outsourcing approach enables ECAs and MDBs to publicly support sustainable decarbonization while indirectly financing LNG projects.

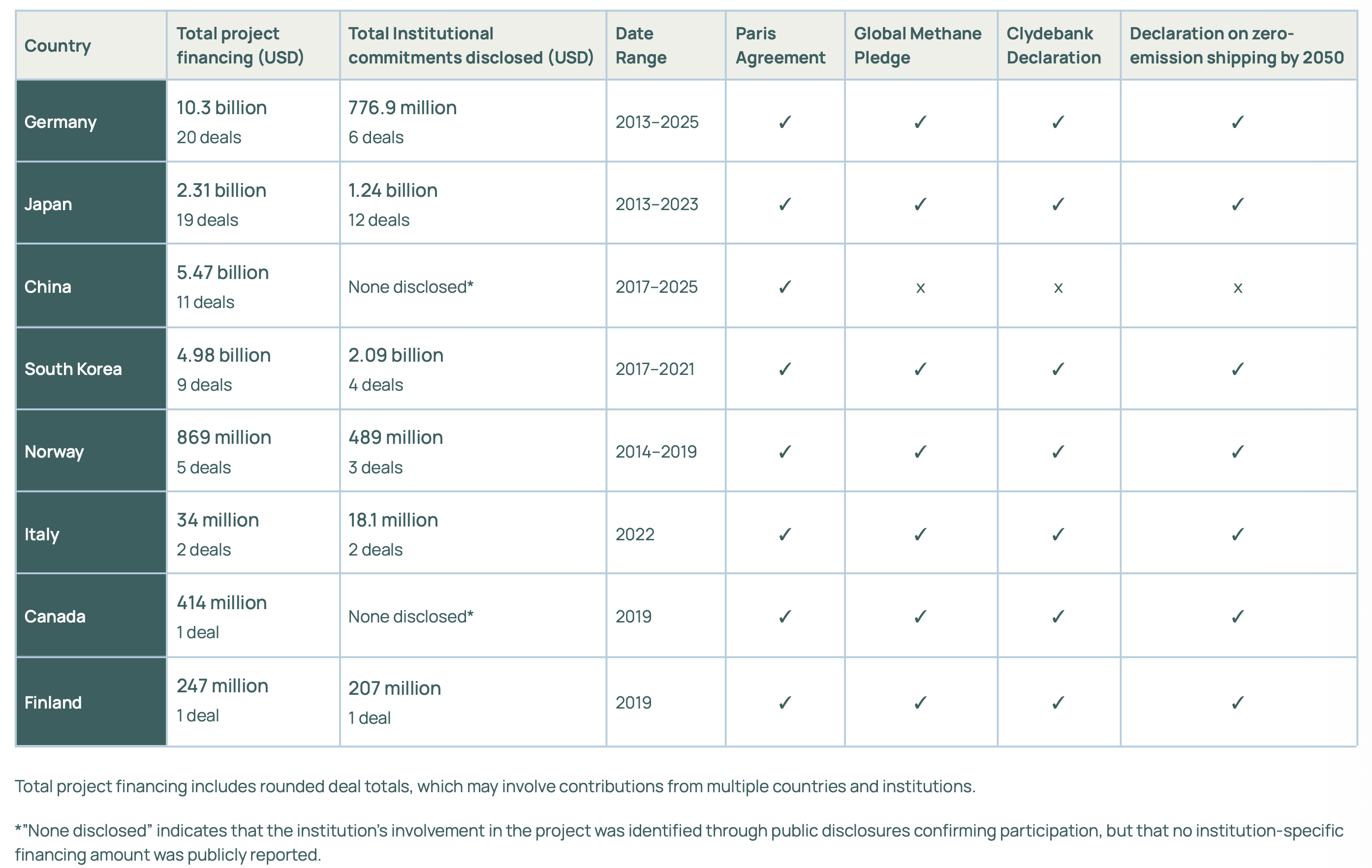

Between 2013 and 2025, over USD 21.9 billion was poured into maritime LNG projects via 76 deals backed by PFIs. Public financiers considerably contributed to this via financial mechanisms including equity, sale and leasebacks, credit guarantees and loans. Assisted by their private intermediaries, PFIs from China, Japan and Germany emerged as top contributors in maritime LNG projects, despite these nations’ commitment to maritime decarbonization initiatives and the Paris Agreement.

These findings reveal an urgent need for greater transparency in shipping finance and the need to address the role of inconsistent reporting, financial intermediary lending and faulty “sustainable” finance frameworks in funding high-emission projects incompatible with decarbonization policies.

Public LNGC Financing in Action: The South Korean Case

LNG carriers are built by shipbuilding companies, often referred to as shipyards. These companies collaborate with end-users and shipowners to construct purpose-built vessels meeting specific needs. Only a handful of shipyards worldwide meet the technical requirements of LNGC construction, which necessitates the usage of high-quality, high-pressure, corrosion-resistant steel pipes and specially built cryogenic cargo tanks designed to store LNG at extremely low temperatures.

Since the 1990s, LNG carrier orders have been dominated by three shipyards operating out of South Korea: Hyundai Heavy Industries, Samsung Heavy Industries and Hanwha Ocean. The country’s comparative advantage and expertise in cryogenic containment systems makes it the preferred choice for LNGC shipowners.

However, while Korea may dominate LNGC construction, it relies heavily on importing key vessel components, including cargo tanks. Korea lacks the necessary technologies to build these tanks at commercial scale and pays billions of dollars in fees to access these technologies from foreign companies. Developing said technologies at home via public-private partnerships is therefore a priority for the Ministry of Trade, Industry and Resources.

Korea provided USD 44.1 billion in LNGC financial support during the last decade. Much of this came from public financial institutions including the Korea Export-Import Bank (KEXIM) and the Korea Trade Insurance Corporation (K-SURE), which provide state-backed financing, guarantees and insurance for LNGC construction.

Between 2015 and 2025, KEXIM provided over USD 27 billion in LNGC financing in the form of loans (over USD 8 billion) and guarantees (USD 19 billion). K-SURE provided USD 6 billion in guarantees, with the Korea Development Bank (KDB) contributing USD 2.4 billion in loans and 8.3 billion in guarantees, mostly directed to shipyards.

Other PFIs participating in shipbuilding include the Korean Asset Management Association (KAMCO), which established a shipping fund to finance LNGCs and provided equity investment via KDB Infrastructure Asset Management, KDB's subsidiary. Similarly, the Korea Ocean Business Corporation mainly concentrates on ship funds and guarantees, as well as buying out old LNG carriers and leasing them to maritime companies.

In typical fashion, the problematic labeling of LNG as a “transition fuel” is reflected in the operations of key Korean players like Hanwha Ocean, which currently adopts the false narrative that LNGCs are eco-friendly. PFIs like those mentioned above use this framing to further enable Korean public LNGC financing. By using public funds to de-risk LNG shipping, Korean public finance – i.e. taxpayers’ money – directly supports global LNG expansion, locking in long-term fossil fuel use despite the country’s climate commitments.

With nearly half of its shipping investments directed towards LNGCs and KEXIM holding over 50% of its portfolio in fossil fuel carriers alone, Korea is disproportionately exposed to demand-side stranded asset risks, faced with a full orderbook despite an existing glut in the LNG carrier market. While Chinese shipyards have slightly eroded South Korean dominance in LNGC construction in recent years, tightening sanctions and investor withdrawals mean Korea still faces severe financial vulnerabilities because of its place in the LNGC value chain. At least for now, Korea remains the world’s leading producer of LNGCs – and therefore bears primary responsibility for the associated carbon footprint. With the current global LNGC fleet emitting around 12.7 billion tons of CO2e each year, that burden is a heavy one.

The Missing Piece

While understanding private capital flows and the de-risking qualities of public finance certainly reveals what enables LNGC expansion, a critical piece of the puzzle remains obscure: who owns these ships?

In our next edition of Explained and the last blog covering LNGC basics, we’ll dive into how LNGC shipowners are perpetuating harm both to the planet and to people thousands of miles away.

Happy reading!

Related insights

Advancing the Transition Away from Fossil Fuels

Key Outcomes from Santa Marta

2026-05-29

Explained: How LNGC Shipowners Fuel Harm Thousands of Miles Away

How the LNGC industry's weak environmental standards are destroying ecosystems and livelihoods

2026-05-13

Miles to be Heard by Those Who Never Had to Live Downstream: UBS' Exposure to Thai Energy Projects Flagged at the AGM

Thai villager carried years of struggle to UBS' doorstep.

2026-05-11

Explained: How Private Banks are Enabling LNG Carrier Expansion

How finance, not demand, is keeping the LNG carrier industry afloat

2026-03-09

Hyundai Has a Chance to Lead Asia’s Auto Transition — But Time Is Running Out

Time is running out for Hyundai to match Its EV success with climate transparency

2025-09-23

World Environment Day, June 5

#BeatPlasticPollution: A Climate Imperative

2025-06-05

Financing the Climate Crisis: South Korea’s Global Fossil Fuel Footprint

The Role of Public Financing Institutions in the Age of Climate Change

2025-06-04

Navigating the Blue Future: SFOC at the 2025 Our Ocean Conference

Busan, Korea (April 28 - 30, 2025)

2025-05-08

What South Korea’s Next President Must Do to Address the Climate Crisis

SFOC’s 10 Climate Solutions

2025-05-02

Retracing the Steps of the LNG Trade: Why Canada's First Nations Came to Korea

The LNG Boom is "Good News"...for Whom?

2025-03-13

True Climate Impact of LNG Carriers

A comprehensive lifecycle emission analysis of LNG, enabled by LNG carriers

2024-10-11

Floating Pipelines Fuelling the Fossil Fuel Crisis: LNG Carriers

2024-09-01